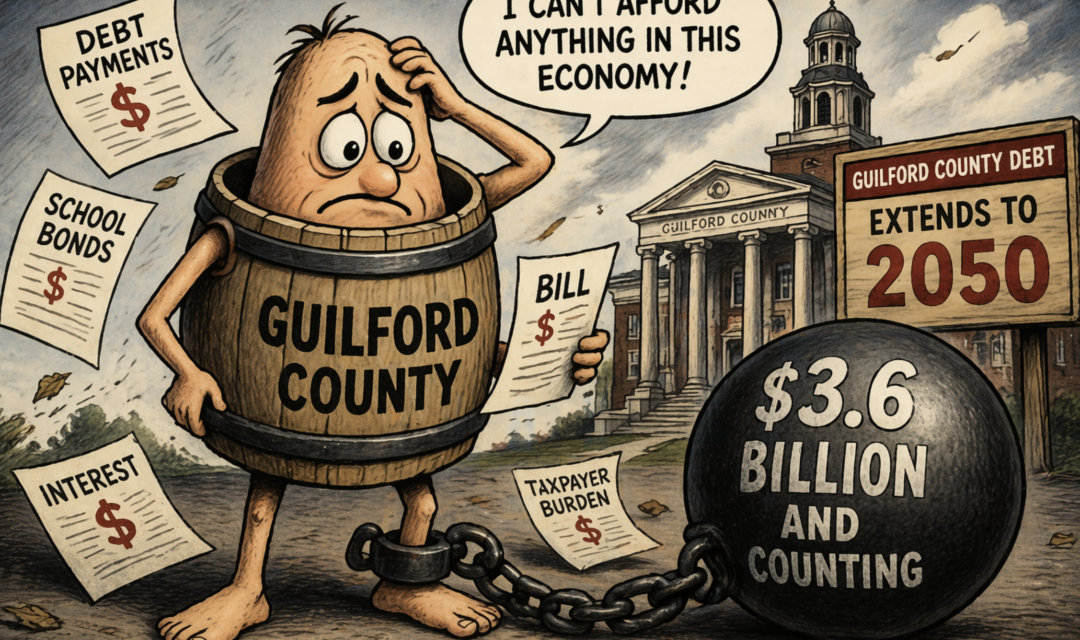

Guilford County taxpayers are on track to repay more than $3.6 billion in debt over the coming decades – a long-term financial commitment that extends to about 2050 under current projections.

And that number is just the current debt. The Board of Commissioners has already been discussing the need for another large school bond referendum down the line because inflation has forced a number of promised school projects onto the cutting room floor, and the board is also considering a downtown campus and renovation project expected to cost more than $170 million that would be added on top of that.

Additional Guilford Technical Community College borrowing is also being discussed, along with other expensive county wants and needs.

That current $3.6 billion total includes roughly $2.38 billion in borrowed money and another $1.13 billion in interest, according to the county’s adopted budget for the fiscal year ending June 30, 2026.

Like with a home mortgage, the county pays interest over time, which significantly increases the total cost beyond the original amount borrowed.

The size and length of that obligation are largely driven by, of course, school construction, which accounts for the biggest share of the county’s borrowing and is expected to keep debt payments elevated for years to come. Each year, the county spends about 45 percent of its total budget on education-related costs, including capital expenditures, operating expenses and school debt repayment.

Most of the county’s debt is tied to projects for Guilford County Schools, with smaller portions going toward Guilford Technical Community College and county government needs such as buildings, equipment and infrastructure.

For the current fiscal year, Guilford County budgeted about $121.7 million for debt service – the annual cost of paying back principal and interest. That growing debt burden is one factor the commissioners are weighing as they prepare to adopt a new budget in the coming months, one which will be based on sharply higher property values following the county’s most recent revaluation.

County officials routinely use debt to fund major capital projects such as new schools, detention facilities, emergency services buildings and other infrastructure.

By borrowing the money upfront, the county spreads the cost over the life of those assets, usually the debt goes out about 20 years.

The largest driver behind the county’s current debt trajectory is the $1.7 billion school bond referendum approved by voters in 2022. The county has already issued a significant portion of that debt, including a $570 million bond issuance in early 2025, with additional borrowing expected in the years ahead.

That $1.7 billion referendum came just two years after voters approved a separate $300 million school bond package.

County projections in the last adopted budget show major future issuances planned for fiscal years 2028 and 2030, which will push annual debt payments higher before they eventually begin to decline.

Under current projections that include both existing and planned borrowing, total annual debt service is expected to rise into the range of $150 million to more than $200 million in the early 2030s before tapering off in later years. That’s money that must be paid each year before spending one dime for core services such as law enforcement, public health and other county operations.

Here’s a scary fact: Guilford County remains below its legal borrowing limit, which means it still has significant capacity to take on additional debt. North Carolina law caps county debt at 8 percent of the total assessed value of taxable property. Under the previous property values, Guilford County’s debt was estimated at just over 3 percent of that total, leaving roughly $3.5 billion in remaining borrowing capacity.

However, the county’s 2026 revaluation increased property values by an average of more than 45 percent. That increase significantly expands the county’s legal borrowing limit, meaning Guilford County could now take on more than $5 billion in additional debt and still remain within state law.

While the county has adopted its own internal debt policies that are more restrictive than state law, those policies can be changed by a vote of the Board of Commissioners. In recent work sessions, the commissioners and staff have explored the idea or doing so.

In addition to school construction, the county uses debt to fund vehicle purchases, public safety radio systems and various county facilities. Some of those purchases are financed over shorter periods, such as four-year installment loans.

Current projections show most of the county’s existing debt being paid off by the mid-2040s. However, when future borrowing is included – such as the continued issuance of school bonds already approved by voters – debt payments are expected to extend to about 2050.

And long before that day arrives, the county will certainly take on additional debt.

{kind=link}